Wealth Management Fees for High-Net-Worth Individuals

By Tess Nakaishi

Updated May 2026

2026 High-Net-Worth Asset Allocation Report

See how 230+ high-net-worth investors with an average net worth of $17M allocate across public equities, private markets, real estate, bonds and cash, including what advised households actually pay for wealth management.

The intricacies of managing significant assets lead many high-net-worth individuals to evaluate working with a wealth management group. Wealth managers specialize in clients at this level and typically offer a wider range of services than a standalone financial advisor, including tax optimization, estate coordination, and access to alternative investments. The question most investors at this stage are actually asking is not what wealth management costs in the abstract, but whether the standard 1% AUM model still applies at their asset level, and whether the planning depth justifies the fee.

Wealth management fees for high-net-worth investors typically range from 0.50% to 1.25% of assets under management, with rates declining at higher asset levels. Across 233 HNW investors benchmarked by Long Angle, the average AUM-based fee is 0.70%, declining to 0.58% above $25M. Roughly two-thirds of advised HNW households pay below 1%, and a growing share have moved to flat annual fee structures.

Key Takeaways

The 1% AUM benchmark is dated for HNW investors. Long Angle's 2026 benchmark of 233 high-net-worth respondents shows an average AUM fee of 0.70%, with the most common single bracket between 1.00% and 1.24%.

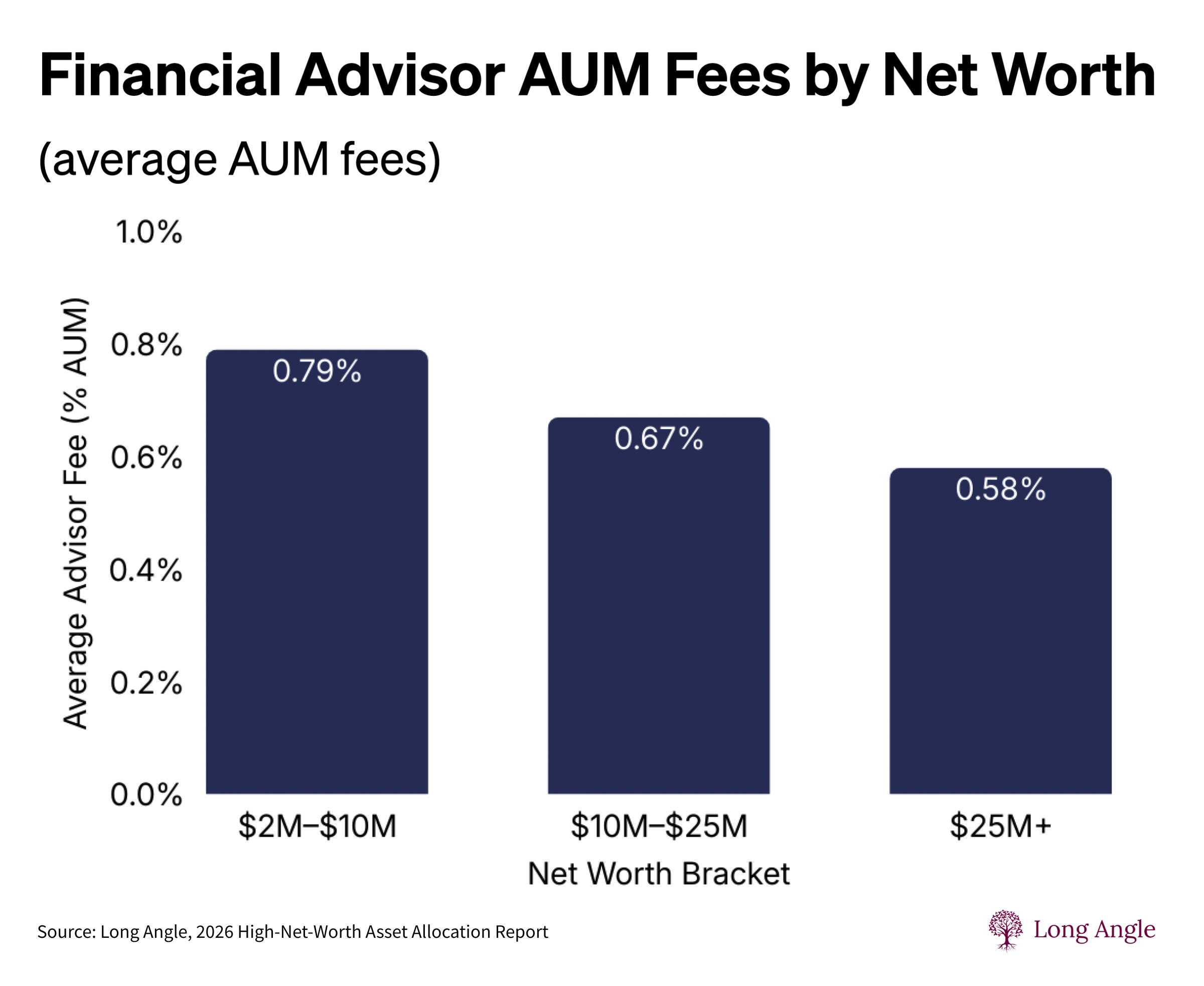

Fees compress as wealth grows. Average AUM fees step down from 0.79% at $2M-$10M to 0.67% at $10M-$25M to 0.58% above $25M.

More than half of HNW investors self-manage. Only 14% have an advisor managing most or all of their assets; 21% of advised households now pay a flat annual fee instead of AUM.

The wealth management market is fragmented. No single wealth manager holds more than a 10% share among advised HNW respondents.

The real question is value, not percentage. HNW investors most often reconsider their advisor when fees compound faster than the planning scope deepens.

How Much Does Wealth Management Cost

The average AUM-based fee paid by HNW investors is 0.70%, with rates compressing from 0.79% in the $2M-$10M bracket to 0.58% above $25M.

What HNW investors actually pay

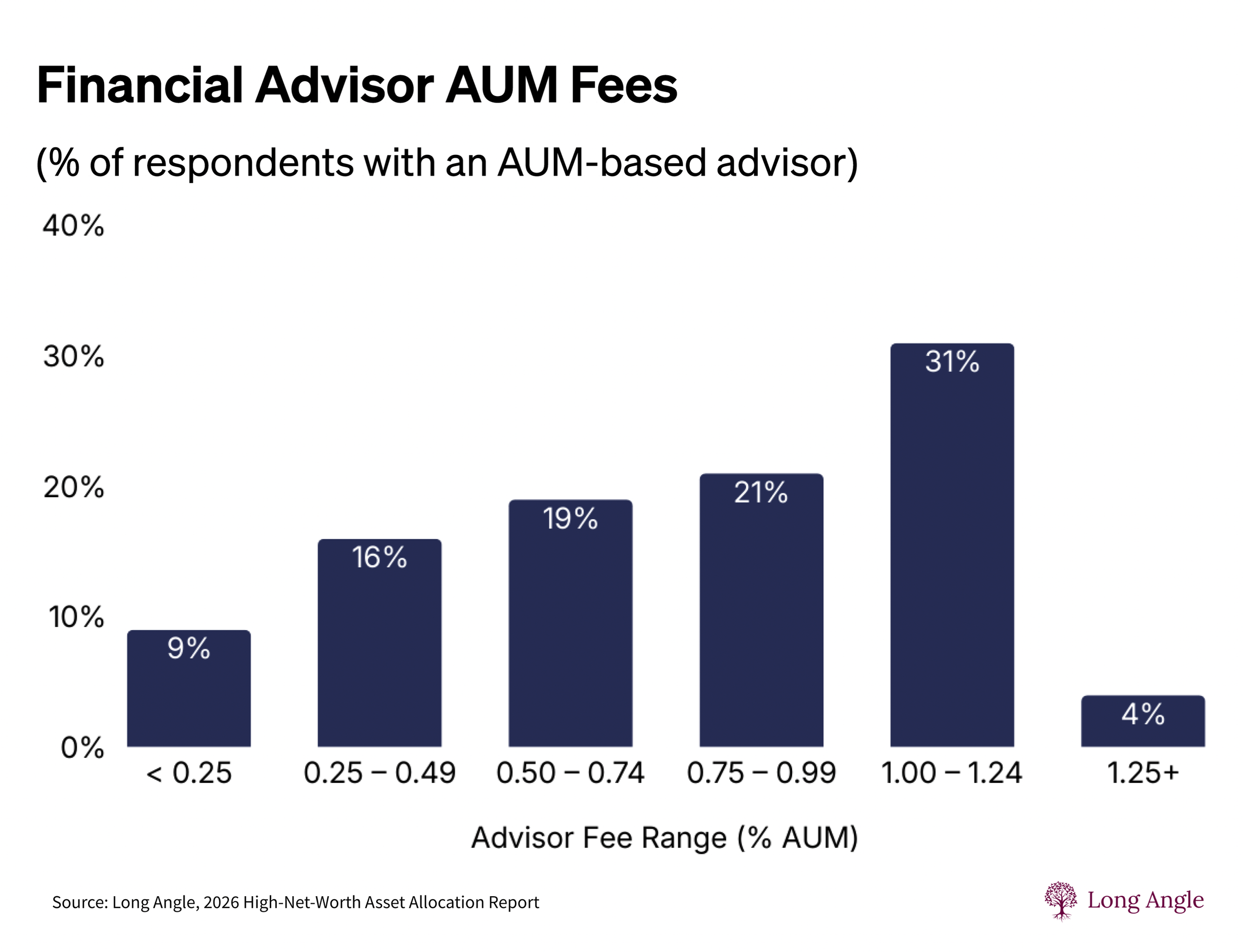

Long Angle's 2026 High-Net-Worth Asset Allocation Report surveyed 233 HNW investors with an average net worth of $17M. Among advised respondents, the average AUM-based fee is 0.70%, with two-thirds paying below 1%. Fees compress as wealth grows: average AUM fees move from 0.79% in the $2M-$10M bracket, to 0.67% in the $10M-$25M bracket, to 0.58% above $25M. The most common single fee bracket reported is between 1.00% and 1.24% (31% of advised respondents), but a meaningful share fall well below that range, including 9% paying under 0.25% and 16% paying 0.25% to 0.49%.

Financial Advisor AUM Fees, share of respondents with an AUM-based advisor. Source: Long Angle, 2026 High-Net-Worth Asset Allocation Report.

The legacy 1% benchmark reflects how the wealth management industry has historically priced its services for affluent clients generally, not how HNW households at $5M and above tend to be priced in 2026. Larger portfolios typically meet asset thresholds at which advisors apply tiered schedules. Some firms publish those schedules openly; others negotiate them on a relationship basis. According to Vanguard's Advisor's Alpha research, the value an advisor can add through behavioral coaching, tax-aware investing, and disciplined rebalancing is typically estimated at around 3% per year, a framing that has shaped how advisors justify their fees, but one that depends entirely on whether the relationship actually delivers on those functions. The SEC's RIA disclosure framework requires registered investment advisors to itemize their fees in Form ADV Part 2A, which is the document HNW investors should request and compare across any firms under consideration.

For larger portfolios, even a tier-compressed rate can compound significantly over time. The compound cost is where most reconsideration of an existing relationship starts.

Alternative Wealth Management Fee Structures

Twenty-one percent of advised HNW households now pay a flat annual fee rather than a percentage of assets under management.

Before comparing fee structures, the terminology is worth disambiguating. "Fee-based" is a broad compensation model that includes any fees paid by clients, which can include AUM fees and even commissions. "Fee-only" is a narrower category that excludes commissions entirely. Within fee-only, the structures that come up most often in HNW conversations are AUM-based, flat annual fee, hourly, and plan-only or subscription models. Members researching alternatives to a traditional 1% AUM relationship often start by asking for a "fee-based" advisor when what they actually want is a fee-only flat-fee or hourly arrangement. The distinction matters because the term "fee-based" alone does not rule out the same compensation structures the investor is trying to move away from.

The shift toward flat-fee structures is no longer hypothetical at the HNW level. Twenty-one percent of advised HNW households in Long Angle's 2026 benchmark now pay a flat annual fee rather than a percentage of assets. The math becomes increasingly favorable as portfolios grow: members report flat annual fees in the range of $10,000 to $15,000 for full-service relationships at $10M and above, which translates to an effective rate of 0.10% to 0.15%, well below the tier-compressed AUM benchmark of 0.58% above $25M.

Members who have made the switch most often cite the same structural reason: when planning fees are separated from investment compensation, the planner's incentive aligns with the quality of the advice rather than the volume of assets gathered. The trade-off is also named honestly. Flat-fee or plan-only structures can leave gaps in ongoing portfolio monitoring and rebalancing unless the relationship is paired with clear check-in cadence or self-managed execution. The decision is whether the savings justify the additional work the investor takes on, or whether to pair a flat-fee planner with a separate execution structure.

For HNW investors with concerns about wealth management fees stacking up, starting with a flat-fee advisor for an initial consultation can be a useful middle ground. The conversation establishes objectives and portfolio allocation before committing to an ongoing management fee. Depending on the results, the client can then make a more informed decision about whether a recurring AUM relationship adds enough value to justify the cost.

| Fee Structure | AUM Fee Range | Flat Fee Example | Services Typically Included |

|---|---|---|---|

| Percentage-Based (AUM) | 0.25% to 1.25%; HNW average 0.70% | N/A | Portfolio management, tax optimization, estate coordination, alternative investment access |

| Flat Fee | N/A | $10,000 to $50,000+ per year depending on scope | Comprehensive planning; investment implementation varies by contract |

| Hourly or Plan-Only | N/A | $300 to $500+ per hour, or $5,000 to $10,000 per plan | Specific deliverables: financial plan, equity compensation strategy, liquidity event planning |

| Hybrid | Tiered; portion managed, portion self-directed | N/A | Mix of ongoing AUM management with self-directed brokerage; reduces total fee burden |

Beyond Wealth Newsletter

Weekly perspectives on money, meaning, and the decisions that come after the financial ones get easier. Read by founders, executives, and investors navigating the same questions covered in this post.

Are Wealth Management Fees Worth It

For HNW investors, the fee question is most often a value question. The percentage matters less than whether planning scope matches the cost.

Among HNW investors, the fee question is most often a value question. The percentage matters less than whether the scope of planning matches the cost. Members who have switched wealth managers typically describe the same pattern: the AUM fee was acceptable until the planning depth stopped keeping pace with the complexity of their situation, at which point the conversation shifted from "what does this cost" to "what am I actually getting."

What HNW investors at this stage tend to want modeled goes well beyond portfolio allocation. Aging parents, multiple children, education planning, angel investing capacity, charitable giving thresholds, equity compensation strategy, and the question of how much room remains for an opportunistic move like a franchise purchase or a private deal, these are the questions a wealth manager's planning function is expected to answer at this level. When the relationship delivers on that scope, the fee is rarely the issue. When it doesn't, the fee becomes the issue quickly.

The compound cost of an AUM fee at HNW asset levels is where most reconsideration starts. Members who have switched describe the math in dollar terms rather than percentages. Annual AUM fees in the $40,000 to $60,000 range are common at $5M to $10M in managed assets and at 0.70% to 0.85% rates. Two to three years of those fees can accumulate well past $100,000, money that, in the framing one member used, is no longer working for the investor. Projected over a typical wealth management relationship of 10 to 15 years, the cumulative cost of even a tier-compressed AUM rate runs to several hundred thousand dollars. The decision is rarely whether the cost is real. It is whether the relationship delivers planning depth that justifies it.

There is a sharper way to frame the same math. Without withdrawals and at the same underlying growth rate, an AUM fee compounds against the portfolio every year, which means the effective cost over a working lifetime can be expressed as a percentage of the final portfolio value. A 0.25% AUM fee over a 55-year horizon costs roughly 14% of the final portfolio. A 1% fee costs closer to 73%. This framing oversimplifies in two ways worth naming: it assumes no tier-stepping as the portfolio grows, which most firms apply automatically as assets cross published thresholds, and it does not adjust the tier thresholds for inflation, which means the savings from tier-stepping are often less than they appear on a nominal basis. Even with both corrections applied, the directional point holds. At HNW asset levels, the percentage you pay annually is also a meaningful percentage of what your heirs eventually receive.

Long Angle's benchmark data shows the tier-stepping pattern clearly.

Financial Advisor AUM Fees by Net Worth, average AUM fees by household net worth bracket. Source: Long Angle, 2026 High-Net-Worth Asset Allocation Report.

Negotiation room expands with asset level. At $2M and above, most independent RIAs have room to come down from their published schedule. At $5M and above, that room becomes substantial. At roughly $10M and above, the major private wealth platforms become willing to move toward 0.50%, which aligns with the broader benchmark tier of 0.58% above $25M. Long Angle members who have negotiated successfully describe two patterns: published fee schedules are the starting point, not the ending point, and the negotiation is usually most effective when paired with a specific articulation of what the investor expects the advisor to deliver beyond portfolio management.

With that framing established, the benefits of working with a wealth manager are worth naming directly:

Planning depth that integrates the whole household balance sheet. Tax planning, estate coordination, equity compensation strategy, charitable giving, and liquidity planning evaluated as one system rather than in isolation.

Convenience. Wealth management for high-net-worth individuals is time-consuming. Depending on personal interests, lifestyle, and availability, outsourcing the ongoing work to a competent firm can be worth the cost on time alone.

Objectivity. A wealth manager can assess the numbers without the personal bias that often shapes household financial decisions. This matters most during high-stakes moments such as estate planning, business sales, or major intergenerational conversations.

Integrated services. Tax planning, bill payment, estate management, direct indexing for tax-loss harvesting, and access to private investment opportunities can justify higher fees when the investor would otherwise need to coordinate multiple specialists separately.

Access to private funds and alternative investments. Wealth managers can sometimes provide access to private markets not readily available to individual investors.

The maturity of the flat-fee alternative also depends on the scope being sought. Flat-fee financial planning relationships are increasingly accessible at the HNW level. Flat-fee full-service wealth management, meaning integrated planning, investment management, tax coordination, and estate strategy under a single fixed fee, is meaningfully thinner. Members who want only the planning function generally have more choice than members who want the full wealth management scope but without an AUM-based fee. This gap is real and worth naming when evaluating alternatives.

There is also the option to take a hybrid approach, with some managed assets covered by a wealth manager and other holdings in a self-directed brokerage account. By lowering the amount of managed assets, a lower fee tier may become feasible, and the overall fee burden across the household balance sheet can be materially reduced.

The decision to switch wealth managers is also not purely economic. Some members run the math, evaluate the alternatives, and still stay with their existing AUM relationship, sometimes because the relationship has accumulated value the spreadsheet does not capture, sometimes because the cost of friction in changing a working arrangement exceeds the fee savings. The math says what the math says. The actual decision factors in continuity, trust, and what the existing advisor knows about the household that a new relationship would have to relearn. Both directions are defensible. What members consistently regret is staying with an arrangement they have already decided is wrong.

Where do HNW investors actually source the wealth managers, CPAs, and insurance specialists they trust?

Long Angle members nominate, pilot, and benchmark vetted partners across financial products, tax, residency, and insurance. The selection process is documented: 20+ member pilots, scored ratings, direct comparisons, no placement fees. Members access the partners with the work already done.

Wealth Management Frequently Asked Questions

The questions HNW investors most often ask when evaluating wealth management fees fall into a consistent pattern.

What do wealth managers do?

Wealth management services typically span estate planning, financial planning, investment management, property planning, philanthropy, retirement planning, tax services, and legal coordination. The defining feature is integration: a wealth manager treats the household balance sheet as one connected system rather than addressing each domain in isolation.

What's the difference between AUM fees and flat fees?

AUM fees are calculated as a percentage of the assets your advisor manages, typically ranging from 0.50% to 1.25% at HNW levels. Flat fees are a fixed annual amount, usually negotiated based on scope of work rather than portfolio size. The structural difference matters: AUM fees scale automatically as wealth grows, which can compound costs even when the advisor's workload stays the same; flat fees decouple the cost of advice from the size of the portfolio, but typically require clearer specification of what's included.

Wealth managers vs. financial advisors: what's the difference?

Both financial advisors and wealth managers provide financial advice, but "financial advisor" is the broader umbrella term that includes wealth management as a subset. Financial advisors work with clients across a wide range of income and net worth levels. Wealth managers specialize in more complex financial situations and HNW to ultra-high-net-worth clients. Because of this, wealth management fees tend to be higher than what generalist financial advisors charge, though the integrated scope is also broader.

Can you negotiate wealth management fees?

Yes, fee negotiation is standard at HNW asset levels. While 1% remains the legacy benchmark, HNW investors regularly negotiate other payment structures or lower percentages. With alternatives such as robo-advisors generally charging 0.25% to 0.50% and flat-fee planners offering integrated services at materially lower effective rates, wealth managers have become increasingly willing to negotiate. Best practice is to ask a potential advisor to demonstrate the value they will provide and why the fees are appropriate given the services offered. Confirm which assets are being covered, what's included in the fee, and whether tiered pricing applies as assets grow.

What should you consider before switching wealth managers?

Three considerations come up consistently in peer discussions. First, terminology: confirm whether the new advisor is fee-based or fee-only, since "fee-based" alone does not rule out AUM or commission structures you may be trying to move away from. Second, scope: define what you actually want the advisor to do, planning only, investment management, tax coordination, or all of the above, before comparing fees, because the fee comparison is only meaningful once the scope is matched. Third, exit math: calculate the after-tax cost of leaving your current arrangement, particularly if you hold proprietary funds, complex products, or concentrated positions with significant unrealized gains. Members who have switched also recommend vetting the advisor's interview process and confirming that the new advisor's plan lives in updatable software, so periodic check-ins extend the original work rather than restarting it.

How do you choose a wealth manager?

HNW investors typically vet wealth managers across reputation, experience, fee structure, scope of services, and fit with their specific household complexity. Long Angle members who have evaluated wealth advisors recently consistently recommend three practices: clarify scope before evaluating fees, request references from clients with comparable situations, and confirm the structural details of the relationship including how the plan gets updated, how often check-ins occur, and what happens between sessions.

Customizing Wealth Management

The right wealth management fee structure depends less on the percentage and more on what the investor needs the advisor to deliver beyond portfolio management.

The decision to work with a wealth manager, and at what cost, ultimately depends on individual needs and priorities. For some HNW investors, the integrated planning, tax coordination, and estate strategy offered by a full-service wealth manager justify the AUM fee. Others find value in a more à la carte approach, hiring specialists as needed on an hourly or flat-fee basis and self-managing the investment side.

Whether opting for a traditional percentage-based fee, a flat-fee arrangement, a plan-only relationship, or a hybrid setup, the discipline is the same: define the scope first, evaluate the fee against that scope, and revisit the arrangement when the situation changes. What HNW investors at this stage are paying for is integrated judgment across a household balance sheet that has grown more complex, not portfolio management in isolation. The fee structures that work best are the ones that match the depth of work actually being performed.

At this asset level, the fee question is rarely about the percentage. It's about whether the advisor across the table has actually worked with someone in your specific situation.

Long Angle is a vetted community where high-net-worth members share what they're paying, who they're using, and whether they'd hire that firm again. The environment is solicitation-free, no salespeople, no commissions. Recommendations come from peers who have personally engaged the same advisors, CPAs, and wealth management firms you're evaluating.

More From Long Angle

Beyond Wealth Newsletter

Long Angle's free weekly newsletter covering wealth management, investing and life at the intersection of money and ambition. Subscribe »

Navigating Wealth Podcast

The Long Angle podcast. Founders and executives on the financial and personal decisions that matter most. Listen »