The Best Credit Cards for High-Net-Worth Individuals

Looking for a trusted network of high-net-worth peers? Apply now to join Long Angle, a vetted community of high-net-worth investors, entrepreneurs, and professionals. Access confidential discussions, live events, peer groups, and private market deals.

Table of Contents

Credit Card Features

What is the Best Bank for High-Net-Worth Individuals?

The 5 Best Credit Cards for High-Net-Worth Individuals

Credit Card Diversification

How to Optimize Credit Card Use

The Bottom Line: What is the Best Credit Card for High Earners?

Approaching even seemingly simple decisions with an eye for long-term rewards is often the key to successful wealth management and growth. Consider the choice of what credit card (or cards) to use.

High-net-worth individuals have the option to pick between exclusive luxury credit cards that come with stricter requirements and higher annual fees or more modest cards that still offer incredible value. Those seeking elite status and the most premium perks might opt for an invite-only credit card, such as the Amex Black Card.

Generally, high-net-worth individuals are less concerned about factors such as interest rates when selecting a credit card and more interested in cash back, points, miles, and other perks. As such, the best credit cards for high-net-worth individuals are typically those offering the most value tailored for the cardholder’s specific needs and interests.

Credit Card Features

Different features will matter most depending on individual lifestyle. Here are a few elements to keep in mind when shopping for high-net-worth credit cards:

Cash Back vs. Points

Many high-net-worth individuals prefer cash back for its simplicity and universal value. For example, the Wells Fargo Active Cash card offers a flat 2% cash back return, providing straightforward rewards without the need to chase sign-up bonuses or optimize spending categories.

That being said, points or miles are advantageous for those who travel frequently, as points often translate into higher travel rewards compared to cash. Credit cards like the Chase Sapphire Reserve and Amex Platinum have excellent travel perks, including access to lounges and significant point multipliers on travel expenses. While points and miles are a bit more complicated to navigate compared to the simplicity of cash back, they are a worthy consideration for travel enthusiasts.

There is no right answer here; 59% of Americans with net worths over $1 million own cash-back credit cards, while 49% have travel rewards cards. In comparison, 72% of Americans with net worths under $1 million have cash back cards, versus 23% with travel cards.

Convenience

Being able to request higher limits via a phone call, rather than having to unlock or unfreeze credit, reduces the hassles associated with managing credit. Good customer service, of course, goes a long way, and many premium credit cards offer concierge service.

Fees

Some credit cards come with hefty annual fees. For high-net-worth individuals, these fees might be nominal given the benefits offsetting the cost (particularly for those who travel frequently), but higher annual fees may not be worth it for those unlikely to take full advantage of the accompanying perks. The American Express Platinum card, for example, has an annual fee of $695.

Other Perks

Credit cards for high earners often come with plenty of additional benefits, such as:

Welcome bonuses

Travel protections

VIP event access

Airport lounge access

Credits or discounts for retail, dining, transportation, etc.

High-Net-Worth Asset Allocation Report

Long Angle's annual high-net-worth asset allocation report presents the latest investment trends and strategies for portfolios ranging from high-net-worth to ultra-high-net-worth investors.

What is the Best Bank for High-Net-Worth Individuals?

High-net-worth individuals will want to get their credit cards through reputable banks that can support their financial needs, often opting for private banking divisions.

Some favorite banks for high-net-worth individuals include:

Bank of America

Chase

Citigold

JP Morgan

Goldman Sachs

Morgan Stanley

The 5 Best Credit Cards for High-Net-Worth Individuals

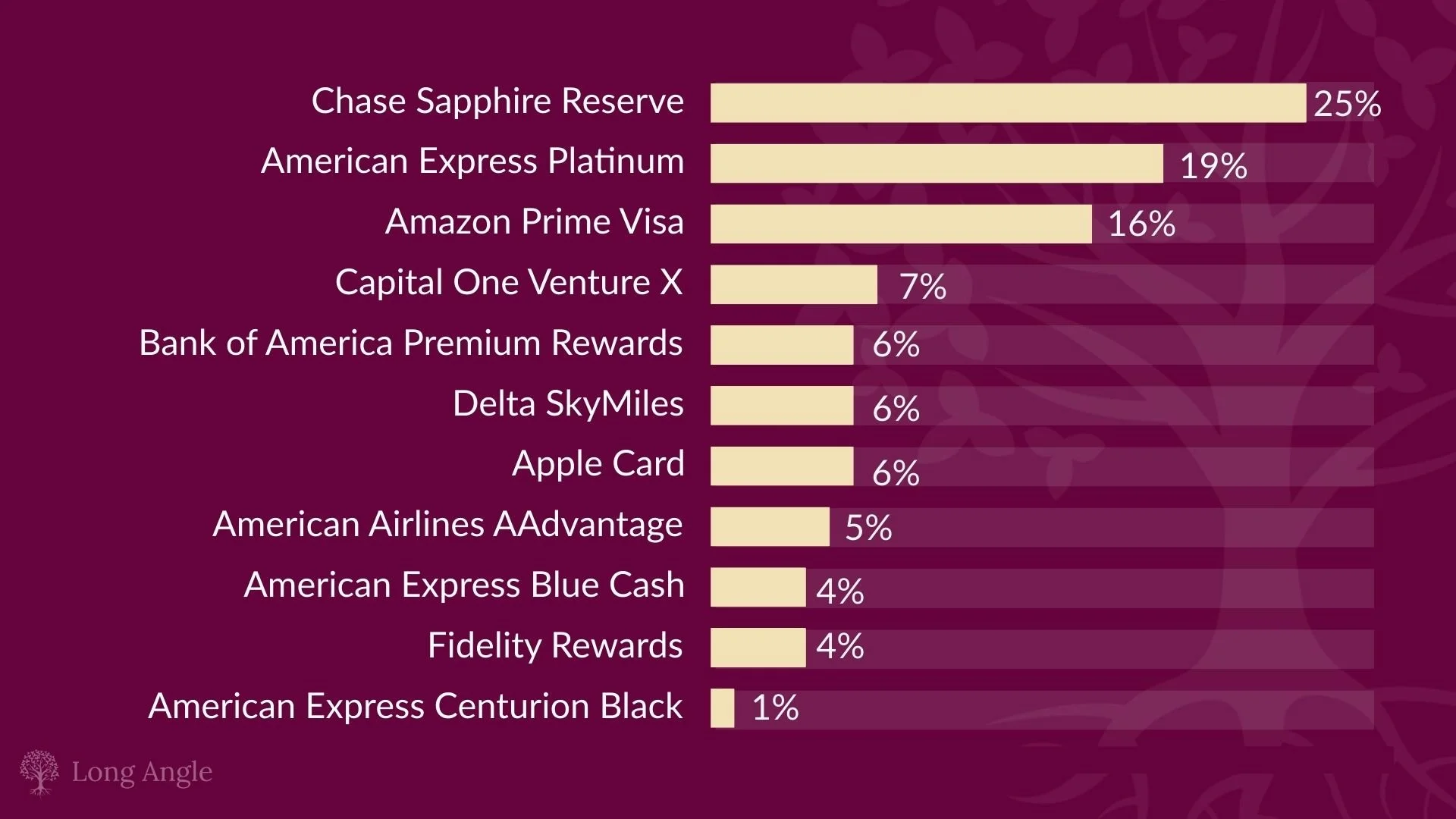

Long Angle polled its high-net-worth community to ask about preferred credit cards for the wealthy. The top five most popular choices (discussed in detail below) were:

Chase Sapphire Reserve

American Express Platinum

Amazon Prime Visa

Capital One Venture X

Bank of America

Chase Sapphire Reserve

The Basics:

Annual Fee: $550

APR: 22.49%-29.49%

Sign-Up Bonus: 60,000 points (after spending $4,000 on purchases in the first 3 months)

Perks:

3x for travel/dining, 1x on all other purchases, or 10x for hotels and car rentals booked through Chase Travel and 10x for Chase Dining

Annual $300 travel credit

$1,000 in partner value

Global Entry or TSA Precheck or NEXUS credit

Access to Sapphire lounges (over 1,300 worldwide)

Book through The Edit for premium hotel perks

Rental car discounts and upgrades

Travel perks such as lost luggage reimbursement and roadside assistance

Complimentary Doordash subscription

10x points on Lyft rides

10x points on Peloton purchases

1:1 point transfer

Cons: Highest rewards rates when booking through the Chase portal

Best for: Frequent travelers who want simple redemption options

American Express Platinum

The Basics:

Annual Fee: $695

APR: 21.24% to 29.24%

Sign-Up Bonus: 80,000 points after spending $8,000 in first 6 months

Perks:

5x travel points, 1x points on all other purchases

$200 hotel credit

$240 digital entertainment credit

$155 Walmart+ credit

Airport lounge access

Hotel benefits

Premium car rental privileges, including car rental insurance

VIP experiences at events such as Wimbledon and the Kentucky Derby (note: card just provides access to buy tickets for these events)

Concierge service

Cell phone protection

Automatic credits, such as $200 a year for incidental airline fees and $200 a year for Uber

Global Dining Access by Resy

Cons: One of the highest annual fees. Have to prepay hotels via Amex and book flights through Amex to redeem points.

Best for: Frequent travelers willing to spend more on annual fees for exclusive perks

Amazon Prime Visa (Through Chase)

The Basics:

Annual Fee: $0

APR: 20.49%-29.24%

Sign-Up Bonus: $200 Amazon gift card when you sign up, 0% promo APR

Perks:

5% back at Amazon and Whole Foods

5% back on purchases through Chase Travel

2% back on restaurants, gas stations, and local transit

1% back on all other purchases

10% back on rotating Amazon Prime purchases

Travel perks such as roadside dispatch and lost luggage reimbursement

Referral bonus (up to $500 in Amazon gift cards per year)

Cons: Must have Amazon Prime membership ($139 annually)

Best for: Those who frequently shop at Amazon and/or Whole Foods.

Capital One Venture X

The Basics:

Annual Fee: $395

APR: 19.99% - 29.99%

Sign-Up Bonus: 75,000 miles after spending $4,000 on purchases in the first 3 months

Perks:

10x miles on hotels and rental cars, 5x miles on flights when booked through Capital One Travel, 2x for everything else

Annual bonus of 10,000 miles

Airport lounge access

$300 annual credit for bookings through Capital One Travel

TSA PreCheck/Global Entry statement credit (up to $100)

Hertz President’s Circle status

$100 experience credit when booking with the Premier Collection

Hotel benefits, like an experience credit, room upgrades, and more

Price drop protection for flights

Capital One dining and entertainment perks

Complimentary membership to the Cultivist

Cell phone protection

Cons: Need to book travel through Capital One to earn miles

Best for: Frequent travelers looking to earn miles

Bank of America Unlimited Cash Back Card

The Basics:

Annual Fee: $0

APR: 19.24% to 29.24%

Sign-Up Bonus: 0% intro APR for 15 billing cycles, $200 bonus after spending a minimum $1,000 in first 90 days

Perks:

Unlimited 1.5% cash back on all purchases

Cash rewards don’t expire

Bank of America Preferred Rewards® members earn 25%-75% more cash back on every purchase, depending on tier (can earn up to 2.625% cash back)

Flexible redemption options

Fraud and overdraft protection

Free access to updated monthly FICO score

Cons: 3% foreign transaction fee

Best for: Customers looking for a flat cash back option

| Chase Sapphire Reserve | Amex Platinum | Amazon Prime Visa | Capital One Venture X | Bank of America | |

|---|---|---|---|---|---|

| Annual Fee | $550 | $695 | $0 | $395 | $0 |

| Sign-Up Bonus | 60,000 points (after spending $4,000 on purchases in the first 3 months) | 80,000 points after spending $8,000 in first 6 months | $200 Amazon gift card when you sign up, 0% promo APR | 75,000 miles after spending $4,000 in first 3 months | $200 bonus after spending $1,000 in first 90 days |

| Perks | 10x for hotels/car/dining through Chase portal, 1x on other | 5x travel points, 1x points on all other purchases | 5% back at Amazon/ Whole Foods/Chase Travel, 2% on restaurants/gas/transit, 1% back on other | 10x miles on hotels/rental cars, 5x miles, 2x everything else | Unlimited 1.5% cash back |

| Reward Form | Points | Points | Cash back | Miles | Cash back |

| Catch | Highest rewards rates when booking through the Chase portal | Have to prepay hotels via Amex and book flights through Amex to redeem points | Must have Amazon Prime membership ($139 annually) | Need to book travel through Capital One to earn miles | 3% foreign transaction fee, best rates for BoA Preferred customers |

| Best For | Frequent travelers who want simple redemption options | Frequent travelers willing to spend more on annual fees for exclusive perks | Those who frequently shop at Amazon and/or Whole Foods | Frequent travelers looking to earn miles | Customers looking for a simple flat cash back card |

Credit Card Diversification

For those looking for simplicity and ease of use, sticking with cards like the Chase Sapphire Reserve or the American Express Platinum will provide the best benefits with the least amount of hassle.

However, others enjoy the fun and strategy of mixing different lines to find the best combination. While this can be a meaningful hobby for some, it might be too time-consuming and cumbersome for others.

Still, a smart mix of cards optimizes rewards across different spending categories. For example, a high-net-worth individual might use the Chase Freedom Unlimited for everyday spending and the Amex Gold for dining and groceries. For those serious about maximizing value, starting with two credit cards is a good rule of thumb. Those interested in multi-card portfolios might also consider cards specific to airlines, hotels, or other brands.

How to Optimize Credit Card Use

Here are some strategies that help high-net-worth individuals get the most value out of their credit cards:

Take advantage of credit card sign-up bonuses and large-spend bonuses. Some recommend opening new credit lines fairly frequently to capitalize on intro offers.

When booking a flight using points, go through the airline directly.

To get the most value out of point deals, it helps to have flexibility in travel plans. For example, Chase offers great options for last-minute travel.

You get the most value out of using points on flights versus lodgings.

Keep in mind options around transferring points. For example, the Bilt Rewards card can be used to earn points on mortgage payments, which can then be transferred to preferred airline partners.

Paying taxes using credit cards can reap big rewards.

Tools such as Mint, Empower, and Lunch Money allow cardholders to auto-sync various cards into a single feed, making it easier to manage them simultaneously.

Take advantage of referral bonuses. For example, existing Sapphire Preferred or Reserve cardholders get 10,000 bonus points for every accepted applicant (up to 75,000 points a year).

Stay up to date on how much points and miles are worth.

The Bottom Line: What is the Best Credit Card for High Earners?

High-net-worth individuals have the advantage of accessing premium credit lines tailored to their unique needs and lifestyles. The key is to align these choices with personal preferences and financial strategies, whether that means prioritizing travel rewards, cash-back benefits, or exclusive perks like concierge services and VIP event access. Each card offers distinct advantages, so determining the best credit card for high-net-worth individuals depends on analyzing spending habits and long-term goals.

To participate in discussions on topics like these with like-minded peers, join Long Angle and connect with a diverse community of high-net-worth individuals. In addition to peer networking opportunities, members also get access to curated investment opportunities and exclusive events.

Looking to expand your investment network?

Join Long Angle, a private community of high-net-worth investors. Together, we leverage our collective expertise and $30B in assets to access, diligence, and underwrite institutional quality alternative investments.